NEWS & KNOWLEDGE

Interesting things about the packaging industry, retailing dynamics, consumer trends and NOA’s insight.

The real and ongoing impact of COVID on trends within the paper packaging sector

The real and ongoing impact of COVID on trends within the paper packaging sector

With vaccination rollout well underway and, in the UK at least, industry beginning to emerge from the pandemic, what will the longer-term effects be on the paper packaging sector?

At NOA, as leading analysts of paper packaging trends, we’re frequently being asked if and when the high demand for paper-based packaging will level out.

We all know demand has increased. Ecommerce, already on the march, has grown exponentially during the pandemic, with bricks and mortar stores continuing to close, and doorbells across the country ringing to the sound of the ecommerce delivery driver, with yet another cardboard box.

But let’s take a more careful look at what is happening currently before we examine the longer term.

The paper packaging sector has had an unusually busy time and demand for raw materials, be that for flat board for the carton industry, or reels of paper for the corrugated industry, has risen.

It’s a simple rule of economics, but of course as demand begins to outstrip supply, so prices of the raw material goes up. There has been anything between three to five different increases in the last five or six months, equating to between 20% and 40% overall.

Demand for pallets for delivering goods on has also shot up. Plus, there’s a shortage of construction materials – cement, timber and so on – which is also adding to the pressure on the supply of pallets, which are, of course, made of wood and nails. In consequence, pallet prices have roughly doubled over the last five or six months.

High demand for paper has increased lead times. For a sector renowned for its responsiveness, to have a lead time of, in some cases, three months is almost unheard of. While these lead times are beginning to ease back, they are still extended.

And there are other factors affecting the current state of the paper packaging market.

The nationwide shortage of qualified HGV drivers is having a significant impact. With headlines like Lorry driver shortage threatens Haribo sweets and Lorry driver shortage: UK government and retailers in emergency talks, it’s clear that there is something of a crisis, with not enough drivers to transport goods around the country and across borders.

We even hear that fresh produce deliveries are now being affected because there aren’t the drivers left to deliver fruit and vegetables to all our stores across the UK. We may see shops with empty shelves simply because the produce is stuck in a regional distribution centre.

There had been a driver shortage in the UK for some years, aggravated by Brexit. COVID has just made a bad situation worse.

Add to this, what is being dubbed the ‘pingdemic’, with businesses struggling to cope with so many employees having to self-isolate, the situation doesn’t look likely to ease for some months to come.

And let’s cast our minds back to the heavily laden container ship blocking the Suez Canal in March – an example of shipping’s effort to keep up with demand. It had a knock-on impact on the supply chain, as too are the problems currently being experienced at Chinese ports, which are becoming congested in part due to China’s anti-COVID measures which are in turn hampering logistics activities.

This, in a nutshell, is where the paper packaging sector stands today: demand has expanded, but supply and logistics haven’t. While on the surface it looks like the paper packaging sector has been making hay while the sun shines, in reality this boom in demand has been tempered by high paper prices, high pallet prices, shortages in supply, and the logistics and shipping sectors on their knees.

Let’s now return to the question of what will happen to demand in the paper packaging industry. Our packaging industry research is spotting these trends.

First, the frenetic activity for online ordering, while it will continue to rise, won’t do so at such a rapid rate. The current rate that online sales represents in the UK has grown over the last 2 years and is likely to ease over the next 12 month period. The rate of increase for MODIE (the category for online corrugated packaging that NOA uses in their reports for Mail order, Distribution, Internet & eCommerce packaging) will cool from current figures (+15% month on month) and drop back to a new, post-Covid level (estimated at +10%), over the period of the next 12-18 months as the rise of the “Fusion Shopper” grows in today’s radically changed retail scene.

Second, the green agenda is snapping at the heels of plastic production. The SUP (single use plastic) directive is coming into play. This was enshrined into EU law in 2019, abolishing certain single use plastics by 2022/2023, and the UK is adopting this directive.

This is driving OEMs to move out of using expanded polystyrene packing, in particular electrical goods, such as fridge distribution, high-tech computing equipment, etc.

Consumers are increasingly keen to see alternative packaging in place and, with COVID easing, are turning their minds once again to the green agenda.

All this is driving real innovation in the sector. Our report Changing Dynamics in the UK Sheet Plant Market 2020 revealed how this particular sector in the UK has come out of the doldrums, through entrepreneurship, growth and innovation.

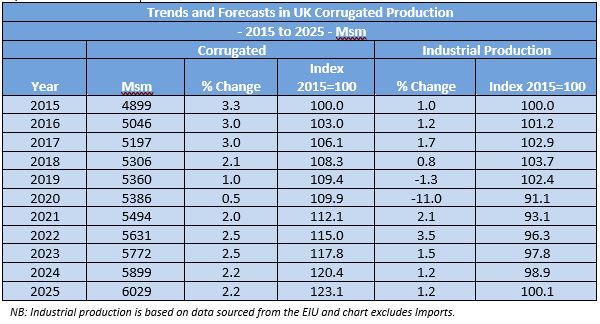

Our estimates at the end of 2020 in our Changing Dynamics in the UK Sheet Plant Market 2020 report were as follows:

In the light of the first 6 months of 2021, where we have experienced incredible demand in both the UK and mainland European markets, our estimates have adjusted notably now. We now see the UK experiencing one of the best years for corrugated demand in a decade with growth rate estimates at this half-year stage likely to be doubling our previous forecasts (for those interested in our latest numbers, please contact us via neil@noa.uk.net).

One innovation we’re keeping a careful eye on is the European market for honeycomb paper-based products. This sector has grown by +15% year-on-year over the last five years and we anticipate it will put on another +20% (YOY) over the next five years. Adoption of honeycomb as lightweight construction materials within the bodywork of Formula 1 cars a few years ago has been mimicked ‘mainstream’ by most European car makers: a remarkable innovation for the paper-packaging industry!

In summary, our packaging industry analysis predicts higher than forecast post-COVID levels of demand for all paper-based packaging. This will be further fuelled by the green agenda, driven itself by legislation and public pressure: top down and top up.

But a word of caution. If the capacity isn’t put on to meet this increased and increasing demand, then alternatives will be sought. Market forces will find other materials, and that may well be plastic.

At the same time, plastic producers are investing heavily in innovations of their own, and promoting their activities, with a fair amount of green-washing – we’ve written about the issues with green-washing too.

So the challenge for the paper packaging sector is clear. The demand is there, and to meet this demand you need to invest, or the demand will go shopping elsewhere.

At NOA, through our packaging market research, we have all the statists and information you need, on which to base any investment decisions. Why not get in touch.

At NOA, we specialise in packaging market research and packaging industry analysis, marketing for the sector and of course – through our MD Neil Osment – one-to-one coaching services at senior level.

To talk to the team please get in touch or email listening@noa.uk.net.